New Year Old Money

Fellow humans,

Yesterday I was sitting and writing in Panera Bread near some older people, and I wasn’t trying to eavesdrop, but they were talking very loudly about ‘Jewish something, Goldman Sachs, and Trump is a liar.’ Before they became too obnoxious though, an employee turned up the music, and their voices were immediately drowned out by indie-sounding tunes. Thank God for music.

You’ve survived another year of sporadic writings filled with unsolicited information and half-decent messages about improving ourselves. For the record, most readers provide no feedback, so although I find the matter amusing, I don’t know if most of you find my work useful or not. I could be publishing into a large void, which works for me, as long as I’m able to continue creating.

Living paycheck to paycheck is not the way we should operate. Working miserable jobs to pay burdensome debts and overpriced bills should not be such a social norm either. When I recall my experiences regarding money, I’m relatively confident in my perspectives, because I know a diverse group of people, so I believe I have a balanced sample of the world’s population.

Growing up in Western Pennsylvania did not expose me to much diversity, but twelve years in the military did. I’ve built solid relationships with people from poverty-stricken West Africa to those who grew up with more money than they knew how to spend. When I look outwards at the world, I’m convinced that I’m seeing reality, and I see most people severely mismanaging money.

Today’s message includes a quick breakdown of my personal finance strategies, which have been working extremely well for the past four years, and were passed along to me from someone else. As I’ve mentioned before in SALtoshi Whitepaper, I was financially irresponsible for many years, but one conversation with one of my military leaders has triggered me to redeem myself.

For a moment, let’s not make such a big deal about the amount of money we earn. We’re no longer living in times when we need large amounts of money to invest, which is the ultimate goal, considering our fatally flawed national currencies (inflation, confiscation, corruption, etc.), and how easy investing has become since the internet and smartphones have gone mainstream.

People often ask me what I do, and rather than mention Bitcoin, my response is usually, “I’m an investor.” The thing about becoming an investor today — once the ball starts rolling, stopping is impossible. I’m not saying investing is only an addiction (it’s addicting), but I’m saying once someone learns how money works, we realize the never-ending movement of money is essential for success.

If we were living 1,000 years ago, then we could probably save gold and silver, and wouldn’t need to diversify our money. However, fiat currencies have since taken over, and have their hooks into every part of our global economy. At first, fiat currencies weren’t such a problem (backed by gold), but have dramatically devolved over the past five decades, so saving dollars is counterproductive.

Furthermore, consumerism and debts exist in abundance today. We waste money on the most unnecessary things, and don’t even get me started on the ridiculous things we finance. Why do we use credit to buy clothes? Anyway, hindsight is 20/20, which shows me how backwards I was for most of my adult life, but instead of beating ourselves up, let’s do something to fix the problem.

The goal is to embrace the new year while pursuing old money. What’s old money? When we stop living check to check, and start saving/investing; our money ages. Hopefully by 2024, all of us will still have some money leftover from 2023, and maybe even from 2022. However, hope is usually not enough to make a difference. We need to play an active role in managing our money.

I think I’ve mastered a few personal finance strategies, which are time-consuming, so whoever starts the process should be committed to keeping detailed records of income and spending, tracking debts, and sacrificing some luxuries. The point is to learn about our financial habits, then attack the problems. Eventually, we’ll have extra money for investing, which is the fun part.

👏👏👏

In a way, I’ve learned to become my own accountant. The goal is to have constant knowledge of our financial situation, in order to avoid overspending, and to know exactly how much money is available for investment. Without this data, which probably applies to most people, we’re taking shots in the dark with our money, and fooling ourselves thinking we might fortuitously become rich.

Three Basic Personal Finance Tools

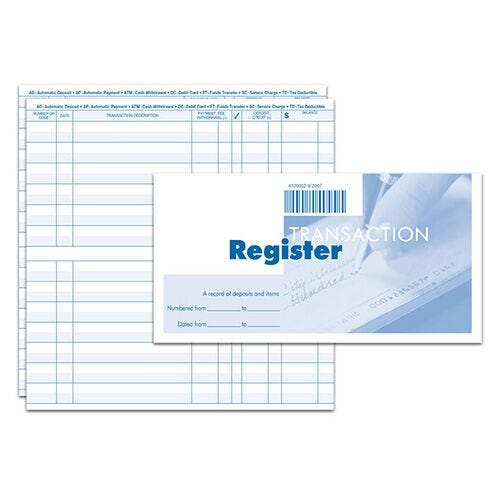

My favorite tool is a spreadsheet which emulates an old-school bank transaction register. I’m sure some of you have received a checkbook for your checking account, and have also received the following booklet. I’ve created a Google Sheet to act as a digital version of the booklet, which is where I track my transactions and bank balances with 100% accuracy.

Not everybody is comfortable creating spreadsheets, but learning is worth the effort, and it’s free with a Gmail account. My spreadsheet is super basic, and does not require advanced skills. Overthinking the process would be a mistake. My way is only one way. As long as we have accurate information about our money, we’re off to a really good start, so everybody can find their own way.

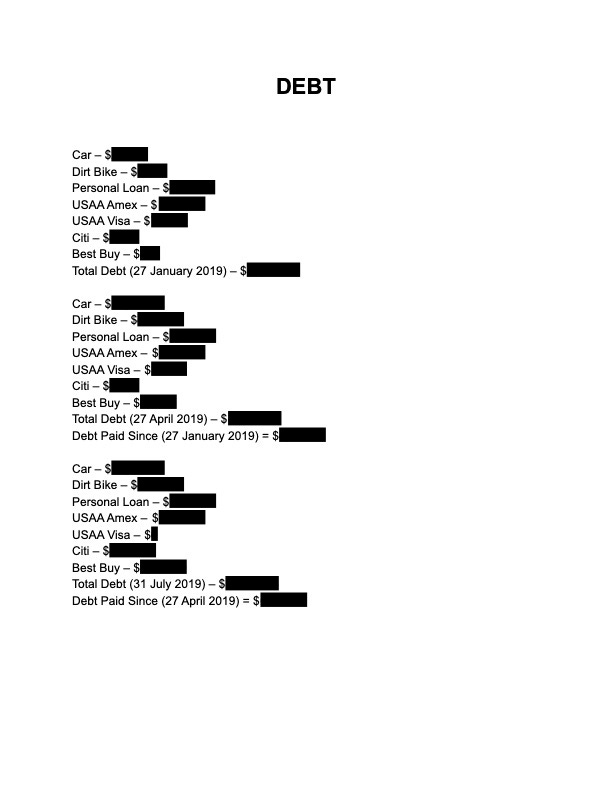

The second tool is a document to track debts. The type of document and formatting is not as important as the information. Simply having all debts listed in one place is key. This document only needs to be updated once per quarter, because debts typically don’t change often. An effective strategy for paying debts is to pay those with highest interest rates first.

Interest rates can be added next to each debt for additional clarity. As you can see (partially), my debts were out of control when I started the process. I was out of control until I started the process. Being organized helps us gain control over any situation, and knowledge is powerful. Ideally, we could pay an accountant to do this type of work, but instead we play the hand we’re dealt.

The third tool is only necessary for people who have a habit of reckless spending. During the beginning, I would do my best to estimate how much money I would need for the following two weeks — such as gas, food, entertainment, even haircuts. Then, I would withdraw an appropriate amount of cash from the bank. No debit or credit card usage. Budgeting 101.

The cool thing about documenting our money is watching it grow (hopefully) over the months and years. Trying to compartmentalize all this information in our brains is setting ourselves up for failure. More documents can be created for other things, such as investment tracking and net worth. Feel free to ask questions. Thank you for sticking around while I geeked out about spreadsheets.

Have a great new year!

Until next time,

Salvatore Norge

P.S. — I’ve read a book years ago which strongly urges readers to pay all debts (except for mortgages and college loans) in full before investing. From my experiences, I would mostly agree.

“Keep falsehood and lies far from me; give me neither poverty nor riches, but give me only my daily bread. Otherwise, I may have too much and disown you and say, ‘Who is the Lord?’ Or I may become poor and steal, and so dishonor the name of my God.” -PROVERBS 30:8-9

I’m not very wise. Never financial advice. Do your research.